Understanding The Cost of An Employee

I would like nothing more than to see all employees, municipal and otherwise, paid in accordance with their value to the community as well as to the organization.

However, that would mean many if not most would be paid well above six-figures. Multiple times for many. That’s not just fire and police. That would include teachers. It would also include that water department worker who comes out at 2 am to fix a water main break when it’s 35 degrees outside with the wind blowing 25+ mph. But that’s just me dreaming and being in deep appreciation for those who watch over and take care of my needs. I was raised in a blue-collar home where it was believed and often said how grateful we should be for having a good, steady job.

There is also another view I take. From the finance viewpoint, those levels of pay would probably not be possible. Ever. Actually, that’s not my real hang up. I am guessing that most people reading this blog have never had to make a payroll out of their own pocket. I have. That’s a completely different world when payroll time comes around at an unbelievably quick pace irrespective of the money you’ve made since the past pay date.

Another point I can’t resist making is that if I am going to get things done through other people, I need them to be there. I’ve seen projects take months that should have been done in weeks. The reason is that it might take the expertise or decision-making skills of 4-5 people meeting together. That’s hard to do with vacations (up to 4-5 weeks!) and holidays and other leave. I have thought many times that if we can do without an employee being at work 9-10 weeks a year, we might be able to do without them for 52 weeks. I’m dead serious.

Let’s look at some of the arithmetic.

Fair warning! If you think I’m exaggerating, you are invited to run these numbers for your own employees. I hope you do.

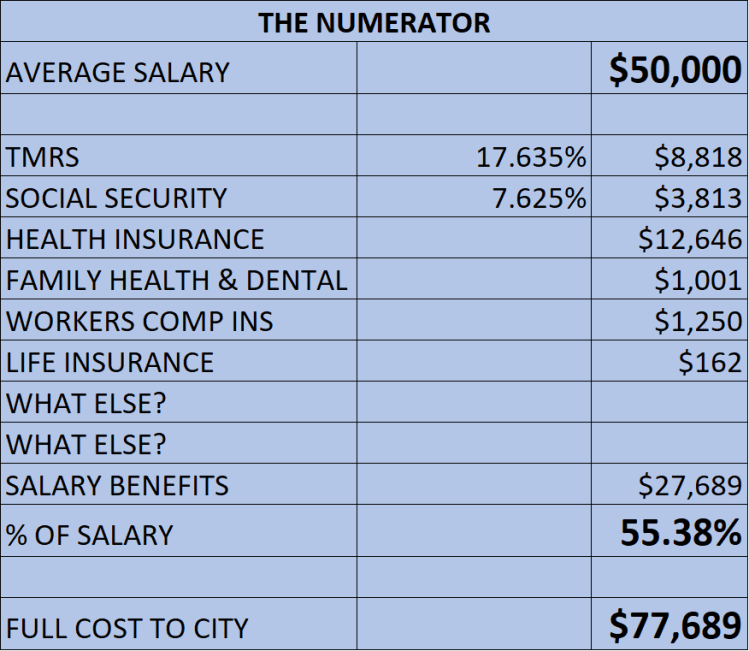

We tend to think of the base salary numbers as the cost of positions. However, depending on your circumstances and offerings, the table below shows how a $50,000 employee may actually cost you and taxpayers $77,689. That’s a 55.38% premium! Worse, most of the salary related costs are not visible to the employee. That’s your fault. Many cities prepare a statement of full costs to hand employees annually. Employees need to know and acknowledge they are aware of the money that is paid out of city bank accounts just for them.

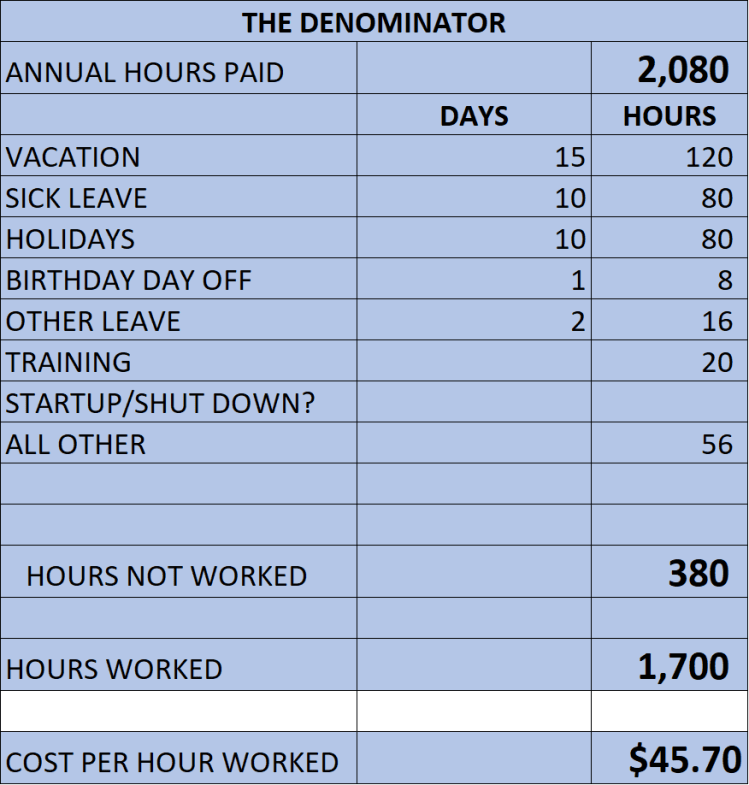

Now that we’ve reality-sized the Numerator, let’s look at the Denominator. Local governments are particularly prone to grant more time-off benefits. It doesn’t show up in the budget even though it should in the spirit of full disclosure. Again, let’s pay a $50,000 employee a total of $77,689 and then tell them their work is not all that critical so they can have more leave and paid to not show up. Sounds a little crazy to me.

Most employees are paid for 52 weeks a year and 8 hours per day or 2,080 hours a year. Yet if we were to deduct for 3 weeks of vacation, 2 weeks of sick leave, 2 weeks worth of holidays and then add another 56 hours for everything else (training, TML, start-up and shut-down time, leaving early the eve of a holiday, etc), we can see how this could add up to about 380 hours off, leaving only 1,700 hours of presumed productivity. I generally use 1,800 hours as a benchmark. What is your hours worked by employee?

How can we preach efficiency and effectiveness and rah-rah about productivity with those kind of numbers? Hold off on your answers. I know them all, and some are legitimate and some aren’t.

The reality is that you could easily have a $50k employee that is costing the equivalent of $45.70 per hour.

One More Day

I know, you want to break out singing the wonderful song from Les Miserables. Sorry, I can’t let you do that right now. Dang! Now it’s stuck in my head.

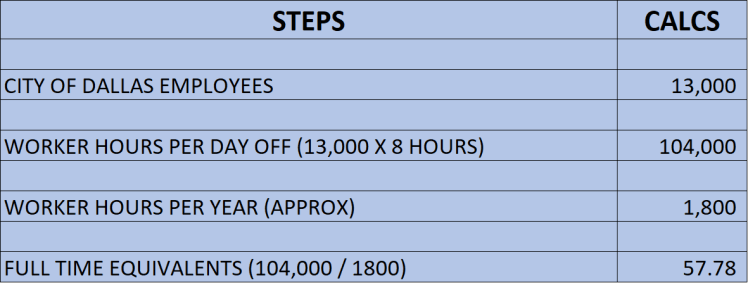

In order to dig a little deeper into the impact of giving employees just one more day off, I’ll pitch out my favorite illustration. Let’s say things are tight, and pay raises are flat. We’ve all been there. We offer employees their birthday off or a National Starbucks day off to stave off a palace revolt. Sounds good.

However, again, if we really give a flip about productivity, let’s paint the reality using the City of Dallas just to create a little drama. Even for Dallas, to instantly plop almost 58 new employees on the scene might cause a few tremors in the foundation of City Hall. Yet, that is exactly the productivity loss by the one-day gift. Do the math on your city. It’s about 0.44 employee per 100 you have now.

Those 24×7 Year-Round Jobs

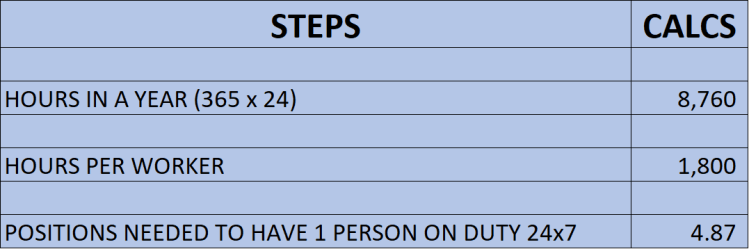

Lastly, let’s look at the impact of coverage for 24x7x365 positions usually found in public safety and a few other areas. In general, given holidays and vacations, it takes almost 5 positions to fill a single position 24x7x365.

Councils need to know these numbers. This is why the cost of a fire station isn’t the big deal. It’s what it costs to staff and equip the functions inside. A similar issue is where it takes a crew of 2-3+ to work on a sewer line. You don’t add 1 person only at a time.

Closing Thoughts

These are just the facts. If you are fretting over any of my individual comments or calculations, just chill. Dwell on the direction and thrust of this blog. I’m just wanting to increase the sensitivity to decisions that are costly and that are easy to grant and impossible to take back. It’s a genuine taxpayer inquiry, and you need to acknowledge that you understand the impact of these decisions, many of which aren’t actually discussed aloud in the public forum.

Employees are very, very expensive. The private sector knows this so well that they can’t move to robotics fast enough. If I can spend $77k x 4-5 worker to compare year-round productivity, and then perhaps look at a life span of a machine being 7 years (just playing with numbers), then I could spend $millions and save tens of $millions if the job could be automated.

But the most costly of municipal jobs aren’t conducive to robotics, right?

Hmmm! I’ll bet those were the very words from private sector workers a decade ago.

Here is my guess. If city management had to make payroll out of their own personal pockets, especially with a 2.5% cap on revenue producing opportunities, and maybe even a share of the cost-saving possibilities, we would see spectacular ideas implemented in a matter of a few years. LFM

You must be logged in to post a comment.