We are blessed in Collin County. The momentum (momo) is enormous, and there are no signs of slowing down. In fact, it is just the opposite. Our momo is gaining momo!

The market value of my property went up 16.90%. Wow! My investment is paying off. My assessed value is lower due to my Homestead and Over 65 Exemption. Still, that’s quite a rise.

The pressure will be on for local government officials to lower the tax rate in most cases. But just how much? It depends. Each government will have to compute an apples-to-apples comparison in accordance with the State’s Truth-In-Tax laws before tax rates are considered beyond July 25, when the Certified Tax Roll is finalized. A key metric is the Effective Rate. The calculation can get complicated, but it basically boils down to this: what is the tax rate that equals last year’s Operations & Maintenance Tax Revenues + this year’s Debt Service obligations?

Oh, by the way, last year’s O&M Tax Rate can be adjusted to compensate for services needed to cover new growth in our community plus anything we annexed. That’s fair. You don’t add $billions in new subdivisions without needing more staff to patrol and serve same.

That basically leaves us with the Revaluations to scrutinized. I made an attempt to separate that critical number from an official document released yesterday by the Collin County Appraisal District that can be found at http://www.collincad.org/downloads/viewcategory/55-estimated-taxable-values.

Can the O&M Tax Rate be dropped by that Revaluation Percentage, which is 5.93% for McKinney and 5.11% for the County as a whole? Not exactly. There are two things not covered in the T-n-T calculation. One is inflation. Personnel costs and just about everything costs more due to inflation. So, there is a reasonable expectation that a portion of the increased tax valuations should cover property service cost increases due to inflation. Inflation means I am buying the same things for a higher price.

So, what should that inflation factor be? The official number is about 2.00%. My expectation is that local government inflation is more due to a fairly large amount of commodity costs, such as fuel, electricity, road materials and more. Let’s use 2.50%, just for illustration purposes.

That would leave about 3.43% in the O&M Component of the Tax Rate for McKinney. Should we expect that level of tax reduction?

Well, maybe, but there is one more thing, and it is not tiny. There are new things needed and approved all the time. Cameras and better police vests are examples. Not cheap. The list is long, and many if not most are new services and service level increases requested by the citizens and taxpayers themselves.

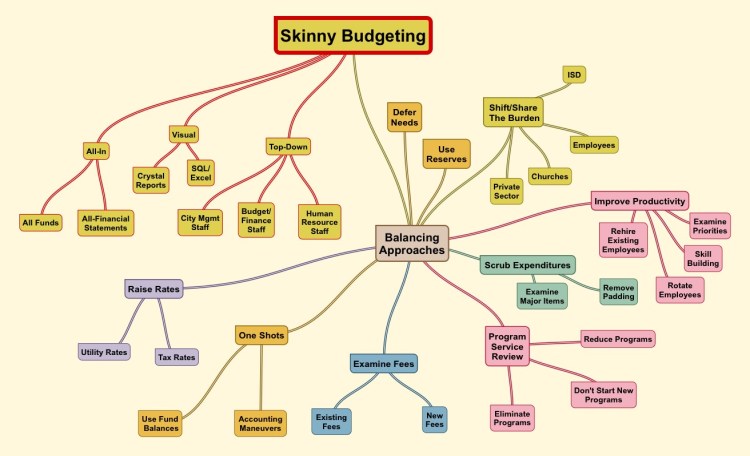

So we should just suck it up and expect all of the 3.43% to be absorbed by local governments? Not at all. In fact, we are isolating just this one component of budget balancing to better understand it. Below the CCAD table, you can find my diagram of all of the other ways local governments have to balance a budget BEFORE they get to raising the taxes or utility rates.

I started calling this approach Skinny Budgeting way before President Trump started using the term. And virtually every avenue for budget balancing has been part of my sermonettes since the early 1970s. The elements of this approach are exhaustive as you drill down within each selection. When I prioritize these approaches, the very last one is to defer necessary expenditures like infrastructure maintenance. The next to the last one is to raise taxes. The very first one is performance improvement, which should be an everyday exercise and not one saved to balance a budget in case of a crunch.

More on Skinny Budget in a later blog. My point for bringing it up as part of this blog is to keep from getting slammed from John & Jill Obvious that tax revenues aren’t the only balancing solution that should be examined.

Also, and this is very important, these CCAD values are preliminary, before they go through the appeal process – a primary obligation of the property owners. LFM