A collaboration between Lewis McLain & AI

A Comprehensive Analysis of the Law, the Politics, and the Reality

For more than a decade, the Affordable Care Act—Obamacare—was the most divisive domestic policy in American life. When Democrats passed the law in 2010 without a single Republican vote, the GOP responded with a unified identity-shaping mission: repeal and replace. For years, “repeal” was not merely a policy position; it was a pledge, a litmus test, and a rallying cry. The House voted more than fifty times to dismantle the ACA. In 2017, with a Republican president and full Republican control of Congress, the party came one dramatic vote away from delivering on that promise.

But the American political landscape of 2025 could not be more different. Today, Republicans do not truly want to kill the ACA—not politically, not strategically, and not practically. The repeal war has ended, not with a dramatic policy reversal, but with a quieter, deeper recognition: the ACA is now woven into the fabric of American life. To understand how this transformation occurred—and why Democrats’ claim that “Republicans have no plan” does not withstand scrutiny—one must examine the ACA itself, the early years of market turmoil, the evolution of public opinion, the GOP’s long list of proposed replacements, and the changing priorities of Republican voters.

I. What the ACA Actually Contains: The Architecture of the Law

The ACA reshaped the American health system through a combination of coverage rules, benefit requirements, financial subsidies, market reforms, and tax changes. Its design is not modular; it is integrated. This complexity makes it extraordinarily difficult to uproot.

The service side of the ACA rests on four pillars.

First, the law introduced guaranteed issue and community rating, which require insurers to accept all applicants regardless of pre-existing conditions and forbid charging sicker people more than healthier ones. This ended a decades-long practice of denying coverage to those who needed it most.

Second, the ACA established a national floor of essential health benefits: hospitalization, maternity care, mental health treatment, emergency services, prescription drugs, laboratory services, pediatric care, rehabilitative therapy, and preventive screenings. These requirements eliminated “junk plans” that appeared inexpensive but failed catastrophically when people became seriously sick.

Third, the law created the Health Insurance Marketplace, allowing consumers to compare standardized plans. Marketplace enrollees receive income-based subsidies that cap how much of their income they must spend on premiums, transforming coverage affordability for millions of low- and middle-income Americans.

Fourth, the ACA expanded Medicaid to low-income adults earning up to 138% of the federal poverty level. Though the Supreme Court made expansion optional, more than forty states ultimately adopted it. Medicaid expansion is now one of the most durable components of the law.

The fiscal side of the ACA includes a mix of taxes, fees, and Medicare savings. The law originally included an individual mandate to encourage healthy people to join the insurance pool. It imposed higher Medicare taxes and a net investment income tax on wealthy households. It added industry fees and reduced certain Medicare overpayments to help finance subsidies and Medicaid expansion. This combination of service and funding mechanisms forms a complex ecosystem—too interconnected to repeal without massive disruption.

While the ACA expanded coverage and standardized essential benefits, these improvements came with a real cost: premiums in the individual market rose sharply in the first several years. Insurers had to cover sicker populations and offer more comprehensive benefits, leading to substantial premium increases for unsubsidized middle-class families. This early cost shock fueled much of the political backlash against the ACA and helped energize the repeal movement.

II. Why Republicans Originally Opposed the ACA

Republicans opposed the ACA for both ideological and structural reasons. They viewed the law as an unprecedented federal intrusion into the health-care marketplace, one that forced insurers to offer government-standardized benefits and compelled individuals to purchase insurance through a mandate. Conservatives argued that these mandates distorted markets, raised premiums for the unsubsidized middle class, and expanded federal authority beyond traditional bounds.

Republicans also viewed Medicaid expansion as financially unsustainable and believed it would trap able-bodied adults in dependency. They argued that the ACA redistributed wealth through taxes on high earners and industries, created new entitlements through subsidies, and imposed costly regulations on employers. In short, to Republicans in the 2010s, the ACA was not a reform—it was an overreach.

III. The ACA’s Market Impact: Early Turbulence, Later Stabilization

The first several years of the ACA were marked by significant volatility. Insurers struggled to price plans because they lacked actuarial data on the newly guaranteed-issue population. Sick individuals enrolled in large numbers; healthy individuals enrolled more slowly. Premiums rose sharply between 2015 and 2017. Several major insurers left state marketplaces, and some rural counties faced the prospect of having only one insurer—or none at all.

The ACA attempted to stabilize markets through three mechanisms: risk corridors, risk adjustment, and reinsurance. But Congress underfunded the risk corridor program, resulting in insurer losses and lawsuits. Reinsurance helped temporarily but expired after three years. Risk adjustment continued to function, but not well enough to offset early turbulence.

However, after the initial shock, the markets stabilized. Premiums leveled off. Insurer participation returned. Marketplace enrollment grew steadily. The Congressional Budget Office reported normalized risk pools. The ACA marketplaces now operate more like mature, regulated utilities than experimental new systems, dramatically reducing the appetite for repeal.

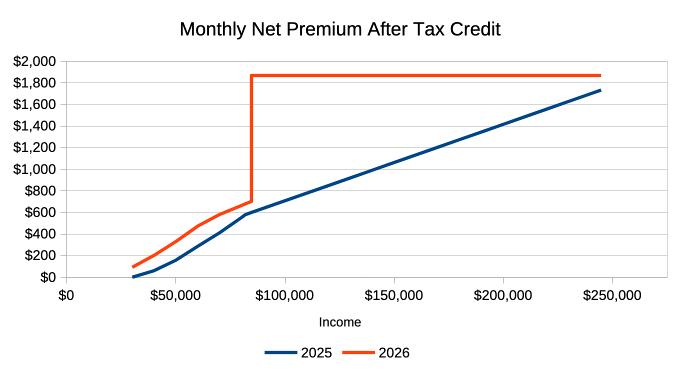

Still, any honest assessment of the ACA must be set against the broader affordability crisis gripping the country. Healthcare and insurance premiums—especially in the individual market—remain among the fastest-rising household expenses in America. Even after the ACA’s markets stabilized, premiums and deductibles remain high for millions of middle-class families who earn too much to qualify for subsidies but too little to comfortably absorb $15,000–$20,000 in annual premiums and out-of-pocket costs. In an era when housing, childcare, transportation, and food are all rising faster than wages, healthcare operates as a second rent payment. The affordability squeeze—felt across red and blue states, among Democrats and Republicans alike—is why the national conversation has shifted from ideological battles over the ACA to a more universal demand for relief. The question shaping the next decade of healthcare will not be repeal or expansion, but whether either party can meaningfully reduce costs for ordinary Americans who feel increasingly crushed by the price of simply staying insured.

IV. Why Repeal Politics Collapsed

The failure of the 2017 repeal attempt marked a turning point. Public opinion had shifted. Millions of Americans now relied on ACA protections, Medicaid expansion, and marketplace subsidies. Parents kept adult children on their plans. Cancer survivors and diabetics could no longer be denied insurance. Small-business owners, gig workers, and early retirees used marketplace coverage as their primary insurance source.

Even deeply conservative states such as Idaho, Utah, Nebraska, Oklahoma, and Missouri adopted Medicaid expansion through ballot initiatives—meaning Republican voters themselves demanded ACA benefits that Republican politicians had long opposed.

The political consequences were immediate. In the 2018 midterms, Republicans lost 41 House seats, driven largely by voters afraid of losing health protections. GOP strategists learned that healthcare repeal was electorally toxic. The repeal war ended not only because the ACA grew popular, but because repeal became a guaranteed losing issue.

V. Why Healthcare Is No Longer a GOP Base-Mobilizing Issue

The Republican Party’s priorities shifted dramatically in the post-2017 era. Voters who once mobilized around healthcare turned their focus toward immigration, inflation, crime, energy policy, foreign competition, and cultural issues. Healthcare—complex, technocratic, and incremental—lost its place as a galvanizing cause.

Many Republican voters now benefit from the ACA themselves. Millions rely on marketplace plans, Medicaid expansion, or pre-existing condition protections. Repealing the ACA would harm their own constituencies—something few Republican leaders are willing to risk.

Repeal also failed to inspire base voters in recent cycles. Unlike border policy or inflation concerns, healthcare does not produce the emotional intensity or visual impact that modern political communication depends on. This change in voter psychology removed the grassroots pressure that once energized repeal efforts.

VI. How Republicans Chip Away at the ACA Today

While Republicans no longer seek full repeal, they continue to reshape the ACA in targeted ways.

They push for broader state waivers that allow alternative benefit designs and relaxed regulatory standards. They promote short-term limited-duration plans and association health plans, which offer cheaper premiums by bypassing ACA benefit requirements. They favor Medicaid work requirements and expanded catastrophic insurance options. They advance large Health Savings Accounts and consumer-directed care models. And through regulatory and budgetary strategies, Republican administrations have adjusted subsidy rules, weakened employer mandates, and reduced ACA administrative infrastructure.

These actions do not dismantle the ACA. Instead, they create a parallel market—leaner, cheaper, and more flexible—that slowly shifts healthier consumers away from ACA-regulated plans, subtly weakening certain parts of the law without openly attacking its core.

VII. Republican Alternative Plans: The Record vs. the Myth

One of the most enduring political claims surrounding the ACA is the assertion that Republicans “never offered an alternative.” This narrative persists because the GOP failed to unify behind one plan, not because it lacked them. In reality, Republicans introduced a long list of comprehensive replacement frameworks.

In 2009, before the ACA passed, Senators Tom Coburn and Richard Burr, along with Representatives Paul Ryan and Devin Nunes, introduced the Patients’ Choice Act, which provided universal tax credits, large HSAs, interstate competition, and state-based high-risk pools.

Representative Tom Price followed with the Empowering Patients First Act, introduced in 2010, 2013, and 2015. This bill contained one of the most detailed conservative health architectures ever drafted—built on age-based tax credits, expanded HSAs, insurance deregulation, state innovation grants, and targeted support for high-cost patients.

Between 2013 and 2016, the Republican Study Committee proposed successive replacement models emphasizing catastrophic coverage, tort reform, association health plans, interstate competition, and state-level innovation. In 2015, Rep. Phil Roe introduced America’s Health Care Reform Act, co-sponsored by over 130 Republicans, combining age-based credits with insurance competition and liability reform.

In 2016, Speaker Paul Ryan unveiled A Better Way, the House GOP’s official healthcare blueprint, which proposed age-adjusted credits, Medicaid per-capita caps, and “continuous coverage” rules.

In 2017, the House passed the American Health Care Act—a full repeal-and-replace bill that would have restructured Medicaid, replaced subsidies with age-based credits, and created a large fund for high-risk pools and reinsurance. Though it failed in the Senate, it was a genuine replacement plan.

That same year, Senators Lindsey Graham and Bill Cassidy proposed a state block-grant system that would convert ACA funding into flexible state allocations, allowing states to design systems of their choosing.

Even after repeal failed, Republicans continued offering alternatives through regulatory reform: expanding short-term plans, association plans, price transparency rules, and catastrophic options. The Republican Study Committee later released its Framework for Personalized Health Care, and the developing 2025 “Freedom to Choose Healthcare” outline continues this lineage.

The historical record is clear: Republicans offered many replacement plans. What they lacked was internal consensus, not ideas.

VIII. The New Republican Reality: Reshape, Don’t Repeal

The Republican Party of 2025 accepts what was once unthinkable: the ACA is here to stay. Repeal is no longer desired, viable, or strategically wise. Instead, Republicans aim to bend the ACA toward a more market-driven system—one with broader choice, fewer mandates, more catastrophic options, expanded HSAs, and greater state control.

The battle that once defined the GOP has shifted. The question is no longer whether the ACA will survive, but how it will evolve.

Conclusion

The Affordable Care Act has moved from controversial experiment to enduring institution. Republicans who once sought its destruction now seek its modification and coexistence. The reasons are clear: the ACA’s benefits became popular, its markets stabilized, its protections hardened politically, Republican voters themselves came to rely on it, and other issues rose to dominate the party’s priorities. The GOP did not lose the repeal war because it lacked ideas. It lost because the ACA became too integrated into American life to uproot—and because no single conservative vision could unite the party.

Today, Republicans are not fighting to kill the ACA. They are fighting to influence what comes next. The battle has shifted from repeal to revision, from rejection to adaptation—a quieter, more pragmatic struggle over the future of American healthcare.

You must be logged in to post a comment.