Written in 1998.

Updated in 2002.

Updated in 2008.

Tweaked in 2016.

Introduction.

The newspapers are full of reports daily. An appraisal district employee is indicted for stealing. A city manager is put on administrative leave while an audit is conducted to determine if his city credit card has been used for personal items over the past few years. A computer analyst is charged with fraud indictment after he allegedly hacked into the District Clerk’s wireless system and “intentionally caused damage without authorization to a protected computer.” A veterinarian, claiming he was fired after complaining about conditions at the city animal pound, wins a $1.2 million jury whistle-blower award.

A former probation officer accused of stealing on the job was placed on probation by a jury, after pleading guilty to felony theft by a public servant. Another paper reports that an audit says the city may have overpaid the law firm hired to collect delinquent property taxes. In another city, a favorable court decision that could cost the city more than $500,000 for more than 200 firefighters continues to smolder as the city looks at appealing the ruling. Another paper reports that an ex-municipal court worker faces charges of tampering with public records – police say he tried to sell fake insurance cards to people with citations. In another city, a former building inspections office employee is charged with stealing more than $20,000 of permit fees. In yet another city, headlines announce that a police sergeant is on leave after a narcotics audit reveals $1,000 is discovered missing.

This little sampling should be quite disturbing to finance officials and city managers for a number of reasons. The first reason is that these are stories from Texas alone. The second reason is that these are stories that have been in the papers in the last 10 days alone! The third reason is that there are probably just as many or even more stories similar to this that have not made the paper in the last ten days. Some of you have reported them to me. Many are handled quietly like is done in the private sector.

There is a fourth reason. Our finance profession knows this reason but doesn’t want to talk about it. Elected officials don’t want to hear about it or don’t care. It is this: stealing is going to rise over the next few years.

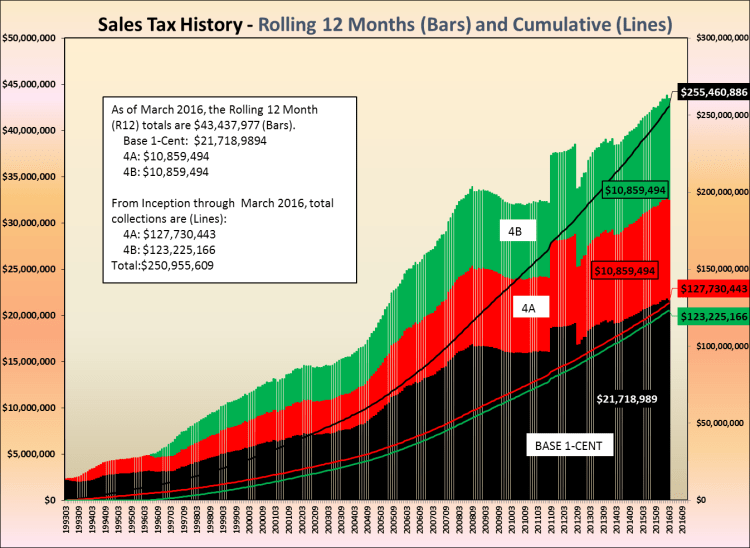

Why? Let’s return to another sampling of the headlines. Actually, I will put the headlines into a succinct composite. Tax bases are slowing or decreasing. Sales tax receipts are plunging. Positions are being eliminated. Pay raises are being canceled or will be minuscule. In some cases, pay may be cut. Employees are going to be asked to pay more of their insurance premiums. Some cities are having some of these budget balancing adjustments placed on them and some are having all of these and even more. It’s not a pretty picture.

But, of course, you are saying this recession is everywhere and is temporary in the great scheme of things. It is even expected and the natural cleansing of the inefficient squeezed down by economic forces. Well, true to an extent. Except things are different now that we have factors induced by national security issues as well as national corruption on an unbelievable and unprecedented scale.

But there is more. A large number of our government workforce has never been through a major cutback. A large number of our city managers and finance officials have never been through this experience – at least not since they have been in the top level positions they now fill. And all of us are just now coming into the realization that we knew would arrive at our doorstep some day: the drill of confronting the results of the Big Lie. The Big Lie is that we can do everything for everybody and, of course, it won’t cost a thing.

How does this become a burden to be carried by finance officers and city managers? And perhaps the connection to stealing hasn’t become clear yet. Let me see if I can make my point. My article entitled “Why Good People Steal” written over four years ago dealt the centrality of dishonesty. It has to do with the rationalization of the mind. We must always be vigilant but really step up our sensitivity when circumstances become ripe for employees to believe in their own minds that they aren’t stealing but only borrowing or getting what is due to them. It is worth replaying the 1998 article and then to add some comments related to 2002 and the next few years that we may be in an economic slump around most of the state.

Why Good People Steal

“Right now — right this very minute — someone is stealing something from the city.” This was the answer to a new finance director’s question about what she should be concerned about in her new role. “And even after realizing this, you cannot become paranoid” was the second part of the answer. She gulped on cue and had that “Bambi in the headlights” look. The answer came from observations over the years and from stories directly shared by finance officials. The focus of this article is not on the method of theft or internal controls, but rather the underlying causes or excuses offered when a theft is discovered. Names of people and organizations are omitted. A couple of examples are even made up for illustration purposes.

The goal is to help you become more effective as a city official by becoming more sensitive to the circumstances that can often lead to a good person making a decision to steal. The emphasis is on “good” people, not the common criminal. This is because rarely will you deal with the latter. It is almost always the former. In particular, a common yet surprising characterization of a person who has been caught stealing is that they were trusted, often long-tenured, and were the last people that would have been suspected of wrongdoing.

The scary part of this topic is not only are good people involved, but much of stealing is petty. That is, the rationalization to steal does not need much effort if the stakes are small. This logic compounds itself if the person initially feels justified due to acceptable standards subtly set in the organization. When an offense is no worse than what someone else does and not any more significant than was done last week or last month, then the stage is set for the rationalizing mind to grant permission for a misdeed. In fact, it is possible that the organization has tacitly given an okay to an act — at least to the person rationalizing in his or her own mind.

Here are some starters:

_ A finance director cannot figure out why 40% of the Scotch tape usage occurs during the months of November and December. Can you help them out here?

_ One city keeps open boxes of coffee packets in the break room but cannot figure out how coffee consumption averages 18 cups per day per employee. Got a clue?

_ An employee makes personal copies at work, which is no worse than the waste of making 100 copies (only $2- $5 worth!) for the weekly office football pool.

_ Employees tend to cash checks at the city collections department after 2:00 p.m. on Fridays because they know their checks will not be deposited until the following Monday.

_ It is general knowledge in some city offices that the department directors instruct their secretaries to make airline reservations for a seat that costs $50-$100 more, but the directors get personal frequent flyer miles for traveling on the costlier airline.

How much worse is each successive example compared to the one before? Are these examples of stealing? Is it an effective use of your time to worry about these little things? Are these bad people? Have you given tacit approval of these acts, knowingly or unknowingly? Do you wish that you had not started reading this article? Are you gulping yet?

I got a call from a finance director asking for help one day. One of his best employees had been caught at a grocery store stealing less than $5.00 worth of products. The city’s policy was automatic termination. The finance director was disappointed because this was such a bright young person with so much promise. The request was to help the young man find some work elsewhere.

The terminated employee came to visit me. He was remorseful beyond description. He had a wife and child and came from a good family. He had shamed them all. He was especially distraught because he simply had no explanation for why he took the petty store products. He had more than enough money in his pocket to pay for the goods. It was a “mental lapse,” he explained.

A city had a loyal employee, a department head over revenue collections, steal over $25,000 during a two-year period. The reason given related to a son going through a divorce needing his help. In another city, a city manager got in hot water for accepting a $25,000 “consulting fee” from a developer on a land deal, a clear impropriety. The reason given was that he had a twin brother who had become addicted to prescription medicine and was in financial straits. He did nothing to help himself, only his brother. See how this works?

A chief accountant, now in jail, was proud to show off his new car. But then his new boat and other things popped up that seemed out of reach for his one-salary. The finance director became suspicious and began digging into what eventually would be revealed as small daily cash thefts that had accumulated to more than $100,000. There was no formal explanation given, but the only conclusion was that his spouse had expectations of a grander lifestyle than is normally afforded a municipal employee.

Another finance director considered a rising star was on her way to her fourth city and a major promotion in stature and a mid-$50’s salary ($100k+ in 2016). Upon vacating her third city, it was revealed that she owed the city several hundred dollars that stemmed from past due water bills for several months. How did that happen? She had instructed the staff to exempt herself, the city manager and the mayor from cut-offs for non-payment, unbeknownst to the latter two, but enough to convince her employees that this was a sanctioned directive.

The finance director acted surprised that her husband had not “taken care of the debt like he was supposed to.” She had just been given her final check with accrued vacation and paid sick leave and another check from her new city for moving expenses — all totaling several thousands of dollars. However, she could only pay half the past due bills — and then that check bounced! After being indicted, she plea bargained just before going to trial and got probation. This one is still a mystery.

One of the highest paid school superintendents in the state has pled guilty to the misappropriation of funds, including purchasing $16,000 of personal furniture for her home with school funds. In another less publicized case, a utility billing manager making over $50,000 was terminated after adjusting her own water bill that amounted to only $30- $50 per month.

What were these people thinking? How could they have possibly rationalized that what they did was okay? How did they think they could get away with it? And in every case, these were considered, bright, trusted and respected people by most of their peers and supervisors. How is anyone supposed to be able to spot these misdeeds or at least suspect that something is amiss before they surface in such obvious ways?

Several municipal officials made a direct or indirect contribution to this article through their stories. There are also some insights that have been forged from their reflections and made a part of this article. They do not desire the focus to be on the person who disappointed them or on the city involved. They do share some advice, along with the author, for the benefit of those city managers and finance officials who not only might become embarrassed by a theft, but who might get their own necks chopped off when a theft occurs.

Be vigilant.

If you do not heed the yellow and red flags of this article, then you may be foolish only up to the moment a discovery is made. Vigilance is the smart substitute for paranoia. Trust your instincts when something does not look right or sound right. Be alert, watchful. Visualize in your mind the ways that money, tools, materials or other city property could be walking off.

Ask questions and walk around with regularity. Listen to cautions made by auditors. Mind the little things. If the organization realizes that little things matter to you, then it follows that larger offenses have commensurate consequences. The most honest person I ever met in government used to keep a can in the copy room labeled, “Personal Copies – $0.10.” He regularly asked with a friendly but serious tone of voice if people were making personal copies on COUNTY equipment and, if so, to kindly make a deposit.

Another finance director tells of her city manager who annually gave the city a check for several hundred dollars marked “for the little things I forgot.”

Open Door Policy.

A city manager was dismayed at what was acceptable by lower echelons of the organization as “authorized” improprieties once it became known that a finance director had instructed or approved a misdeed. The ever so simple solution was to publish a letter annually that, in essence, forbade even the slightest irregularity and personally granted every employee an open door invitation to speak about violations of city policy — real or perceived — with anonymity. E-mail now makes that message even easier to convey.

Changes in Personal Lives – Part I. This advice is offered in the most compassionate manner possible. It can be understood only when you have been faced with a genuinely good employee in crisis who then wishes they could undo a foolish misdeed. You could be doing both the city and the employee a favor if internal controls are stepped up when a person handling money or goods has a crisis going on in their lives. The mind’s ability to rationalize is stretched to its illogical worse state when a spouse has lost their job or has been hospitalized, creating a financial hardship. The burden to make ends meet becomes substantial.

Again, if this advice seems callous, then visualize working the problem backwards. This good person has stolen money, and it is up to you to correct the problem and to possibly destroy their career and lives. IT HAPPENS!

Changes in Personal Lives – Part II. There have been several other stories told with dread over the years that have an especially ugly twist. When you look at the statistics of people in our society with addictions and other personal habits that require sizeable sums of money to sustain, the rationalizations are less honorable yet perhaps even stronger than the ones previously mentioned.

One finance director caught an employee stealing who confessed to a gambling addiction. This thief provided him insight that she, like most gambling addicts, was absolutely certain she had a knack for winning at the gambling tables in Shreveport and Las Vegas. She had just “borrowed” the money with an intention of paying it back with her winnings — winnings that did not materialize.

Another finance official tells of an employee with a drug addiction that quickly grew outside the bounds of affordability for the typical professional salary. One finance official was caught stealing sizeable sums of money after an expensive girlfriend on the side became necessary to hide from his wife. A city manager called me years ago to ask if I thought it was strange that his flamboyant and extravagant assistant city manager over finance had a $100,000 – 2% (this was in the 6-10% days) loan with the city’s depository bank. It is often difficult to spot a questionable lifestyle that could point to malfeasance, not to mention the possible legal hindrances involved in a probe. Ironically, it is often found that many people in this category do little to hide the product of their misdeed. Again, be vigilant and trust your instincts when you sense something is amiss.

Organizational and Personal Clashes.

Back to the less exciting and glamorous signals of conditions that foster improprieties. The ability to rationalize thefts is magnified in some cases when a person justifies the theft as fair compensation. This can be particularly bad organizationally when the city has gone for long periods of no pay increases granted by the city council. It is equally possible to rationalize a theft when someone has been passed over for a raise or has reached the top of their pay range and is no longer receiving pay increases. The signals may be manifested in poor attitudes or other disgruntled actions.

This condition can also occur when there is disillusionment with life in general or with a person’s status in life related to their peers. If mid-life crisis enters the equation and a large percentage of the baby-boomers are into that stage of life, then misplaced justification may grow in the future. The characteristics of the baby-boomers in their 40’s and early 50’s include fewer big increases in income levels, overextended personal debt, high tuition demands for kids in college and increasing requirements to take care of aging parents.

The point being offered is to be sensitive about those who you suspect feel cheated in life or by the organization and who could possibly rationalize that what they are doing is not stealing but righting a perceived wrong.

Conclusion.

It is critical to emphasize the second part of the advice given to the new finance director — do not be paranoid. This article is about the real world and the ugly side of being a financial official or city manager over all departments. On the other hand, it does not apply to most of your employees. It is meant to thrust you into that ugly scene when there has been a theft and to work backwards. If you have not had to deal with a theft in your organization, you are either still lacking experience or missing signals in front of you.

If you can avoid ever having to spend the emotional time and energy working through a theft resolution, then more constructive and rewarding things can be added to your agenda. Most people will vouch that dealing with a theft is all consuming — often for months or years. They also will tell you that it is highly possible that you will get the blame and that you will personally kick yourself for not seeing the obvious or for not trusting your instincts and pursuing your suspicions.

Also, there is a certain amount of effort involved in the establishment of internal controls. You must be adequately staffed in many cases to have effective internal controls. Ironically, many finance officials refuse to ask for justified positions in order to set an example for all departments being denied their budget requests. These sacrifices are all fine until a theft blows up in your face.

I cannot recall a single finance official being thanked for their bare bones budget once malfeasance was pasted across the headlines and embarrassed city officials were looking for heads to roll. So, the perspective is important, the degree of alertness is crucial, the staffing and training for effective internal controls is the fundamental charges for the modern finance official. LFM (1998).

Back To The Future

I had many favorable comments to that article back in 1998. I repeated it again here in 2002, because I think the subject is timeless. As an avid reader of news from every corner of Texas, I can tell you that the frequency of malfeasance is increasing in relatively petty cases as well as with some quite grand.

And what can be more grandiose than the stories that have come out and the stories that continue to come out almost weekly about major misdeeds. They are colossal. It is within the government sector that suspicion has be most prevalent all along. We now know that private sector misdeeds dwarf those found in the public sector – even the largest. But we can find no comfort with that piece of knowledge. We have too many of our own popping up on a regular basis to be smug.

So What Are We Supposed To Do?

This is a hard question to answer and for the answer to apply to everyone. We almost always have to rely on the judgment of the individual to determine what is best under the circumstances. Nevertheless, I am willing to throw out a few suggestions:

Mind your business. This pertains to your shop, your people, their assignments, their level of training, their sensitivity. You cannot be everywhere and check every single thing. You must rely on your immediate fiscal staffers to be deputized to adhere to the most basic practices of internal control. You must be sufficiently staffed and for the staff to be sufficiently trained. A private sector colleague, now deceased, once told me that there isn’t enough money in the paychecks for most finance officials to take the risks they take. You would be well-advised to step up internal control standards, not lower to dilute them.

Work It Backwards.

For motivation to be more vigilant, I suggest you think about how much your next few weeks or months are going to be tied up with a theft if you don’t prevent or discourage theft in all of it many, many forms. Go a step further, however, and assume it is happening. Where is that likely to be? Where do you think it is least likely to be? Call in a few key people and see if you are surprised with how many matches you might find if the question is posed. Involve supervisors dealing directly with money. It would be a healthy exercise just to send the signal through the organization. While you might be surprised with a theft situation, who is sitting next to the person involved in theft who ends up saying “there was something about him …”

Be extra vigilant when you know an employee may be struggling with a personal problem. Send an annual memo that is both a carrot and stick. Include an open invitation but express an expectation that there is a duty involved. You can do this without an Orwellian tone to it. LFM

You must be logged in to post a comment.